- Buy and hold: Buy 3 more cash flow positive properties in high potential areas

- Start property researching in KWC in January / February

- Consider Multi-fam in Q3

- Ron LeGrand's strategy: try 1 or 2 deals to get familiar

- US Real Estate Investment:

- Monitory monthly movements on US real estate markets; focused on Seattle, Bay Area and Miami in Q1 and Q2.

- Detailed investigation in specific neighorhood within 1-2 of the three cities in Q2

Friday, December 31, 2010

Real Estate Investing Goals for 2011

With less than 30 hours to the new year, I have setted the following goals for my real estate investment business in 2011.

Thursday, December 30, 2010

HK Real Estate Bubble?

Many will refer to the CCI (Centa-City Index) provided by Centraline Property http://www.centadata.com/cci/cci_e.htm to assess what cycle time it is for the HK real estate market. Here's the latest chart as of Dec 30, 2010. Overall index is at 87.5, drop 0.9% vs. last week and last month. (Note: 100 = 1997 level).

Clearly, the several recent government policies have halted the rapid upsurge of HK real estate in 2010, driven by hot money rushed in from China and overseas. Whether the 1997 level is the ultimate ceiling or a "new high" will be achieved, that's a million dollar question.

But with cap rate only 2%-4% and such a high risk of downside, I will stay on the sideline until later. HK real estate market is good for speculative short term investors. For long-term buy and hold, i would rather wait for the next cycle.

Another version from commentary in Chinese:

Clearly, the several recent government policies have halted the rapid upsurge of HK real estate in 2010, driven by hot money rushed in from China and overseas. Whether the 1997 level is the ultimate ceiling or a "new high" will be achieved, that's a million dollar question.

But with cap rate only 2%-4% and such a high risk of downside, I will stay on the sideline until later. HK real estate market is good for speculative short term investors. For long-term buy and hold, i would rather wait for the next cycle.

Another version from commentary in Chinese:

Tax implications for renting US property

Recently came across with this article from http://www.snowbird.ca/ that addresses the various tax issues of buying / renting properties in U.S.

Many Canadians own U.S. recreational property near border states. Retired Canadians who are seasonal residents of the U.S., or “Snowbirds” frequently own property in the U.S.

If either of the above situations applies to you, you may be renting out your U.S. property on a part-time or full-time basis when you are not using it. If so, you are considered a “non-resident alien” by the IRS (the U.S. Internal Revenue Service) and you are subject to U.S. income tax on the rental income.

Tax on gross rental income

The rent you receive is subject to a 30 per cent withholding tax, which your tenant or property management agent is required to deduct and remit to the IRS. It doesn’t matter if the tenants are Canadians or other non-residents of the U.S., or if it was paid to you while you were in Canada. The Canada-U.S. tax treaty allows the U.S. to tax income from real estate with no reduction in the general withholding rate. As rental income is not considered to be effectively connected, it is subject to a flat 30 per cent tax on gross income, with no expenses or deductions allowed. The 30 per cent withholding tax would therefore equal the flat tax rate.

Tax on net rental income

Since a tax rate of 30 per cent of gross income is high, you may prefer to elect to pay tax on net income, after all deductible expenses. This would result in reduced–and possibly no–tax. The Internal Revenue Code permits this option, if you choose to permanently treat rental income as income that is effectively connected with the conduct of a U.S. trade or business. You would then be able to claim expenses related to owning and operating a rental property during the rental period, such as mortgage interest, property tax, utilities, insurance and maintenance.

You can also deduct an amount for depreciation on the building. However, the IRS only permits individuals (rather than corporations) to deduct the mortgage or loan interest relating to the rental property if the debt is secured by the rental property or other business property. If you borrow the funds in Canada, secured by your Canadian assets, you would not technically be able to deduct that interest on your U.S. tax return. Obtain strategic tax planning advice on this issue.

Once you have made the election, it is valid for all subsequent years, unless approval to revoke it is requested and received from the IRS. However, you do need to file an annual return.

If you want to be exempt from the non-resident withholding tax and are making that election, you have to give your tenant or property management agent a Form 4224, Exemption from Withholding Tax on Income Effectively Connected with the Conduct of a Trade or Business in the U.S. Contact the IRS for further information.

When you file your annual return, show the income and expenses, as well as the tax withheld. If you end up with a loss after deducting expenses from income, you are entitled to a refund of the taxes withheld. The due date of your return is June 15th of the following year.

It is important to file on a timely basis. If you fail to file on the due date, you have 16 months thereafter to do so. If you don’t do so, you will be subject to tax on the gross income basis for that year, that is, 30 per cent of gross rents with no deduction for any expenses incurred, even if you made the net income election in a previous year. This is an important caution to keep in mind. Many people don’t arrange to have tax withheld at source, or file any U.S. tax forms, on the premise that their expenses exceed the rental income and the net income election is always available.

Filing requirements

You are required to report the gain or loss on sale by filing Form 1040 NR, U.S. Non-Resident Alien Income Tax Return. You would have to pay U.S. federal tax on any gain (capital gain), and if you own the real estate jointly with another person, such as your spouse, each of you have to file the above form. For more information, contact the IRS.

In addition, you would have to report any capital gain on the sale of your U.S. property in your next annual personal tax return filing with Revenue Canada. Remember, you have to report your worldwide income and gains and pay tax on 75 per cent of any capital gain, converted to the equivalent in Canadian dollars, at the time of sale.

Since tax laws, regulations and filing forms can change at any time, make sure you speak to a professional accountant who is skilled in U.S. tax matters.

If either of the above situations applies to you, you may be renting out your U.S. property on a part-time or full-time basis when you are not using it. If so, you are considered a “non-resident alien” by the IRS (the U.S. Internal Revenue Service) and you are subject to U.S. income tax on the rental income.

Tax on gross rental income

The rent you receive is subject to a 30 per cent withholding tax, which your tenant or property management agent is required to deduct and remit to the IRS. It doesn’t matter if the tenants are Canadians or other non-residents of the U.S., or if it was paid to you while you were in Canada. The Canada-U.S. tax treaty allows the U.S. to tax income from real estate with no reduction in the general withholding rate. As rental income is not considered to be effectively connected, it is subject to a flat 30 per cent tax on gross income, with no expenses or deductions allowed. The 30 per cent withholding tax would therefore equal the flat tax rate.

Tax on net rental income

Since a tax rate of 30 per cent of gross income is high, you may prefer to elect to pay tax on net income, after all deductible expenses. This would result in reduced–and possibly no–tax. The Internal Revenue Code permits this option, if you choose to permanently treat rental income as income that is effectively connected with the conduct of a U.S. trade or business. You would then be able to claim expenses related to owning and operating a rental property during the rental period, such as mortgage interest, property tax, utilities, insurance and maintenance.

You can also deduct an amount for depreciation on the building. However, the IRS only permits individuals (rather than corporations) to deduct the mortgage or loan interest relating to the rental property if the debt is secured by the rental property or other business property. If you borrow the funds in Canada, secured by your Canadian assets, you would not technically be able to deduct that interest on your U.S. tax return. Obtain strategic tax planning advice on this issue.

Once you have made the election, it is valid for all subsequent years, unless approval to revoke it is requested and received from the IRS. However, you do need to file an annual return.

If you want to be exempt from the non-resident withholding tax and are making that election, you have to give your tenant or property management agent a Form 4224, Exemption from Withholding Tax on Income Effectively Connected with the Conduct of a Trade or Business in the U.S. Contact the IRS for further information.

When you file your annual return, show the income and expenses, as well as the tax withheld. If you end up with a loss after deducting expenses from income, you are entitled to a refund of the taxes withheld. The due date of your return is June 15th of the following year.

It is important to file on a timely basis. If you fail to file on the due date, you have 16 months thereafter to do so. If you don’t do so, you will be subject to tax on the gross income basis for that year, that is, 30 per cent of gross rents with no deduction for any expenses incurred, even if you made the net income election in a previous year. This is an important caution to keep in mind. Many people don’t arrange to have tax withheld at source, or file any U.S. tax forms, on the premise that their expenses exceed the rental income and the net income election is always available.

Filing requirements

You are required to report the gain or loss on sale by filing Form 1040 NR, U.S. Non-Resident Alien Income Tax Return. You would have to pay U.S. federal tax on any gain (capital gain), and if you own the real estate jointly with another person, such as your spouse, each of you have to file the above form. For more information, contact the IRS.

In addition, you would have to report any capital gain on the sale of your U.S. property in your next annual personal tax return filing with Revenue Canada. Remember, you have to report your worldwide income and gains and pay tax on 75 per cent of any capital gain, converted to the equivalent in Canadian dollars, at the time of sale.

Since tax laws, regulations and filing forms can change at any time, make sure you speak to a professional accountant who is skilled in U.S. tax matters.

Monday, December 20, 2010

Canadian Household Debt - continued

Among all news articles, research and recent speeches of Carney on the issue of Canadian's household debt issue, I found this recent article from CIBC's Avery Shenfeld provides much more indepth perspectives and go beyond the headline number.

Most articles focused on the debt / disposable income %, which currently stands at 145%, a level at par with our counterpart in US.

The most important point Shenfeld made is the distribution of the debt matters.

1. Safe mortgage: For example, the ballooning sub-prime mortgage market that was set up for a run of defaults in US does not seem to exist in Canada. In Canada’s mortgage market, the build-up in debt among those 35 years and over has been concentrated among those with incomes above $50,000 per year.

2. More Prudent Non-mortgage credit: also appears to have been allocated to safer hands in Canada than what we saw in the lead-up to America’s crisis. New credit cards in Canada continue to be issued to consumers with high credit scores, this in stark contrast to conditions in the US prior to the 2008-2009 crisis where a much higher share went to those with low ratings

3. Stronger median incomes: Given that wider gap of the super rich and the rest of population in US vs. Canada, simply looking at the average debt / deposable income of the whole nation might be mis-leading, as the super rich certainly added to the denominator inapproportionally but not to the numerator. Shenfeld considers median income is a more usefule metrics. Labour income growth in Canada has been much more solid than US, and as a result, Canadian median incomes have also seen greater gains than in the US, helping to support domestic household credit performance.

The bottom line is the current pace of debt growth is unsustainable if income growth doesn't catch up. But on the other hand, Canada isn't in the hot water yet.

As for solution, Shenfeld doesn't think sharp debt reduction nor significant rate hikes will be prudent either as that will jeapodize the already weak economy and further damage the export competitiveness. Perhaps as he suggested at the end of the article, the cooling effect of the housing market and declining consumer spending sentiment will gradually reduce the numerator of the equation.

Most articles focused on the debt / disposable income %, which currently stands at 145%, a level at par with our counterpart in US.

The most important point Shenfeld made is the distribution of the debt matters.

1. Safe mortgage: For example, the ballooning sub-prime mortgage market that was set up for a run of defaults in US does not seem to exist in Canada. In Canada’s mortgage market, the build-up in debt among those 35 years and over has been concentrated among those with incomes above $50,000 per year.

2. More Prudent Non-mortgage credit: also appears to have been allocated to safer hands in Canada than what we saw in the lead-up to America’s crisis. New credit cards in Canada continue to be issued to consumers with high credit scores, this in stark contrast to conditions in the US prior to the 2008-2009 crisis where a much higher share went to those with low ratings

3. Stronger median incomes: Given that wider gap of the super rich and the rest of population in US vs. Canada, simply looking at the average debt / deposable income of the whole nation might be mis-leading, as the super rich certainly added to the denominator inapproportionally but not to the numerator. Shenfeld considers median income is a more usefule metrics. Labour income growth in Canada has been much more solid than US, and as a result, Canadian median incomes have also seen greater gains than in the US, helping to support domestic household credit performance.

The bottom line is the current pace of debt growth is unsustainable if income growth doesn't catch up. But on the other hand, Canada isn't in the hot water yet.

As for solution, Shenfeld doesn't think sharp debt reduction nor significant rate hikes will be prudent either as that will jeapodize the already weak economy and further damage the export competitiveness. Perhaps as he suggested at the end of the article, the cooling effect of the housing market and declining consumer spending sentiment will gradually reduce the numerator of the equation.

Ontario Bill 112

Ontario is never a landlord-friendly province. Think how difficult / long does it take to evict a tenant who doesn't pay., the inenforceability of "no smoking" and "no pet" clauses.

Now it's getting worse with the proposed bill 112 that was undergoing second reading.

The Bill makes several amendments to the Residential Tenancies Act, 2006, including the following:

1. The Bill increases the time limit for most tenant and some landlord applications to the Landlord and Tenant Board from one to two years. Tenants can go back in time two years to file a complaint.

2. The Bill requires a landlord who terminates a tenancy for personal use to compensate the tenant and expands the circumstances in which a landlord is required to compensate a tenant if the landlord terminates a tenancy for the purpose of demolition or conversion to non-residential use. Formula given for compensation.

3. The Bill prohibits a landlord from increasing the rent charged to a new tenant by more than the guideline and abolishes landlord applications to the Board for above guideline rent increases where there has been a significant increase in the cost of utilities. No new rent increases to market rent beyond the guideline when you have tenant turnover.

4. The Bill requires that the Board dismiss an application from a landlord who has been given a work order under section 225 of the Act or an order under section 15.2 of the Building Code Act, 1992 and has not completed the items in the work order or the order. Excuse for not paying rent.

5. The Bill requires a landlord to obtain a licence with respect to a rental unit in a residential complex containing six or more rental units in order to enter into a tenancy agreement or renew an existing tenancy agreement. Money grab for Multi-family 6+

Most investors I know, including myself, are just hardworking investors who want to put money into good use. The Bill will simply make investors (local and international) leave and opt for places that offer better landlord protection and more reasonable returns.

Now it's getting worse with the proposed bill 112 that was undergoing second reading.

The Bill makes several amendments to the Residential Tenancies Act, 2006, including the following:

1. The Bill increases the time limit for most tenant and some landlord applications to the Landlord and Tenant Board from one to two years. Tenants can go back in time two years to file a complaint.

2. The Bill requires a landlord who terminates a tenancy for personal use to compensate the tenant and expands the circumstances in which a landlord is required to compensate a tenant if the landlord terminates a tenancy for the purpose of demolition or conversion to non-residential use. Formula given for compensation.

3. The Bill prohibits a landlord from increasing the rent charged to a new tenant by more than the guideline and abolishes landlord applications to the Board for above guideline rent increases where there has been a significant increase in the cost of utilities. No new rent increases to market rent beyond the guideline when you have tenant turnover.

4. The Bill requires that the Board dismiss an application from a landlord who has been given a work order under section 225 of the Act or an order under section 15.2 of the Building Code Act, 1992 and has not completed the items in the work order or the order. Excuse for not paying rent.

5. The Bill requires a landlord to obtain a licence with respect to a rental unit in a residential complex containing six or more rental units in order to enter into a tenancy agreement or renew an existing tenancy agreement. Money grab for Multi-family 6+

Most investors I know, including myself, are just hardworking investors who want to put money into good use. The Bill will simply make investors (local and international) leave and opt for places that offer better landlord protection and more reasonable returns.

Sunday, December 5, 2010

Household debt

People who argue / are hoping for a real estate bubble bust in Canada often use the staggering Canadian household debt to show how unsustainable the mortgage debt level has become.

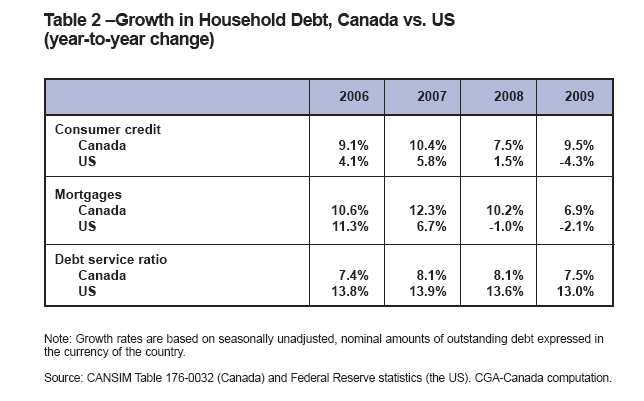

Beyond doubt that the Canadians have been taking advantages of the low interest rate to load up mortgage debtin the past 2-3 years. The following table shows that Canadian household debt continued to increase in 2008 and 2009 while in the U.S. it decreased.

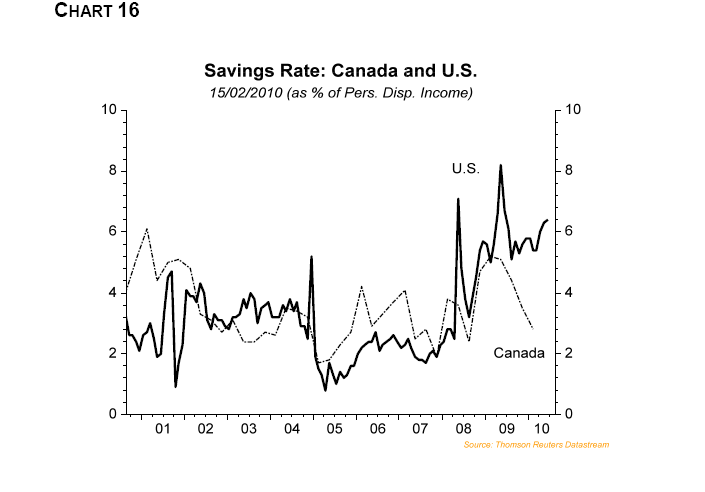

On the other hand, this chart in a report from the Boeckh Investment showns the divergent path for saving rates in the two countries:

Houshold debt as a % of disposable income has risen from the 90% in 1980s to over 145 in 2010.

One piece of good news from the CIBC Benjamin Tal's recent report (June 2010) is the rate of growth has recently slowed down. Tal pointed out the rise in Canadians' credit for the six months ended in March was slower than the expansion of nominal gross domestic product, which include the effects of inflation, and it's the first time in more than seven years that's happened.

With the economic recovery now on solid footing in Canada, Tal said it's positive that the rate at which household debt grows is slowing. He said the recent economic downturn marked the first recession on record in which overall household debt grew.

While debt continues to rise faster than income, Tal said what's more important is that asset levels — which include investments and real estate — are growing at a faster pace than household debt.

Beyond doubt that the Canadians have been taking advantages of the low interest rate to load up mortgage debtin the past 2-3 years. The following table shows that Canadian household debt continued to increase in 2008 and 2009 while in the U.S. it decreased.

On the other hand, this chart in a report from the Boeckh Investment showns the divergent path for saving rates in the two countries:

Houshold debt as a % of disposable income has risen from the 90% in 1980s to over 145 in 2010.

One piece of good news from the CIBC Benjamin Tal's recent report (June 2010) is the rate of growth has recently slowed down. Tal pointed out the rise in Canadians' credit for the six months ended in March was slower than the expansion of nominal gross domestic product, which include the effects of inflation, and it's the first time in more than seven years that's happened.

With the economic recovery now on solid footing in Canada, Tal said it's positive that the rate at which household debt grows is slowing. He said the recent economic downturn marked the first recession on record in which overall household debt grew.

While debt continues to rise faster than income, Tal said what's more important is that asset levels — which include investments and real estate — are growing at a faster pace than household debt.

Thursday, December 2, 2010

Renovation for apartment building

I finally received the Don Campbell's Multi-family investment binder today. I can't wait to review it and learn the best practice. Multi-family units make lots of good sense economically and strategically for one to build out a meaningful portfolio. But of course, buying/owning/managing a multi-family is a whole diffeerent game from that of single-family... as the stake is much higher.

We currently own portion of an apartment bulding outside the GTA. It's a 11-plex in a (i will say regentrifying city). We are definitely learning from our friends on all the best practices step by step.

By googling, I came across this article on Canadian Apartment magazine about renovation for apartment building. It's interesting to note that the higher ROI renovation projects are ceiling fans, W/D machines, computer desk, intrusion alarm, phone line and internet access. While I have heard different opinions on ceiling fans (the major complaint is the liability for landlord in case you tenant make bad use of the fan and injure him/herself). On the other hand, the least ROI projects are screened porch, skylight, and kitchen TV.

We currently own portion of an apartment bulding outside the GTA. It's a 11-plex in a (i will say regentrifying city). We are definitely learning from our friends on all the best practices step by step.

By googling, I came across this article on Canadian Apartment magazine about renovation for apartment building. It's interesting to note that the higher ROI renovation projects are ceiling fans, W/D machines, computer desk, intrusion alarm, phone line and internet access. While I have heard different opinions on ceiling fans (the major complaint is the liability for landlord in case you tenant make bad use of the fan and injure him/herself). On the other hand, the least ROI projects are screened porch, skylight, and kitchen TV.

Wednesday, December 1, 2010

Toronto real estate

Last night, I went for a dinner with a bunch of b-school classmates and someone started the debate about how unsustainable the Toronto real estate market has become and why all of them would remain "renter" until the market cool down. I am always with the view that you buy when you are ready and feel the need, unless you are in the market like Hong Kong where property values have surged 50% since early 2009 (in less than 24 months).

Being an investor myself, I am also concern about the state of health of development here. While looking at the Canada overall, understandabily the overall number is skewed by BC, which accounts for ~15% population. And if you look at affordability across provinces, there are huge differences from Alberta at below 40% to BC at 70%. Ontario and Toronto are both just above 40%, which is anywhere up to 10% higher than the trough but in line with most of the time during the last two decades. Some can argue this number can skyrocket when interest rate jump. But given the currnet state of economy of our country and South of the border, interest rate hike might not happen too soon. From the same report, it's also apparent that though the 40% index in Toronto might be acceptable to users, that will make cashflow positive really difficult to investor. The best range is between 20 - 35 where property values are reasonable but cost of ownership is not too low that end up no one renting in the region.

Another data point from Toronto Real Estate Board shows a even more affodable situation if the data being inflation-adjusted.

Being an investor myself, I am also concern about the state of health of development here. While looking at the Canada overall, understandabily the overall number is skewed by BC, which accounts for ~15% population. And if you look at affordability across provinces, there are huge differences from Alberta at below 40% to BC at 70%. Ontario and Toronto are both just above 40%, which is anywhere up to 10% higher than the trough but in line with most of the time during the last two decades. Some can argue this number can skyrocket when interest rate jump. But given the currnet state of economy of our country and South of the border, interest rate hike might not happen too soon. From the same report, it's also apparent that though the 40% index in Toronto might be acceptable to users, that will make cashflow positive really difficult to investor. The best range is between 20 - 35 where property values are reasonable but cost of ownership is not too low that end up no one renting in the region.

Another data point from Toronto Real Estate Board shows a even more affodable situation if the data being inflation-adjusted.

Wednesday, November 24, 2010

Learnings from our first property

After a couple rounds of renovations (we ended up using 2 contractors as the first firm couldn't finish the job up to the standards we required so we had to hire another firm to complete the job) and tens of showing, we finally rent out both units of our duplex in the downtown.

Several learnings throughout the whole process

1. Be a better negotiator - we bid on this house with $34K below the listing price. We were the only bidder but was "pressured" to up our offer by $2K at the end in fear of losing such a "good" opportunity. Looking back, we could have take more money from the table by going back with an even lower offer (there were opportunities or excuses we could use, such as the seller didn't proivde us certain documentation or bills). Of course, the seller could have decided not to sell too.

2. Inspection report only cover the basic - We have used one of the most famous / most popular firm for the inspection. While the report came back with generally positive comments, there were many qualifiers in what an inspector had done or could comment. A qualified opinion on the wet wall should be intrepreted as a red flag of potentially a mould issue and require further due dilignece.

3. Manage your renovation budget - we originally budgeted for $5K, received quotes adding up $20K and ended up spending ~$15K. Granted, the house is old, no onsuite laundry facilities and dish washer, plus many other things that require potential upgrade. However, we learnt that we have to prioritize our spending, much more so than our home house. At the end of the day, what you want to do is to provide a safe, comfortable living space that looks attractive enough and leave a good first impression with the potential tenants. With that in mind, we crossed out items that are nice to have, but not must have (such as laundry, dish washer, yard), but focus on things that address the safety, comfort and first impression (such as humidifier, kitchen vent, stair, front porch). Plus, you can always leave some of the renovation item when the lease is up for renewal to appeal the tenants to stay for longer.

4. Beware of newly renovated unit - there is always a good or bad reason why the previous owner would spend $$ to upgrade the unit / house. It could be the owner hoping to make a significant premium, or even worse, hoping to cover up issue by some quick fix.

5. Try to get to know the neighbor before you buy - if you can. They are very good sources of due diligence of the current owner

Several learnings throughout the whole process

1. Be a better negotiator - we bid on this house with $34K below the listing price. We were the only bidder but was "pressured" to up our offer by $2K at the end in fear of losing such a "good" opportunity. Looking back, we could have take more money from the table by going back with an even lower offer (there were opportunities or excuses we could use, such as the seller didn't proivde us certain documentation or bills). Of course, the seller could have decided not to sell too.

2. Inspection report only cover the basic - We have used one of the most famous / most popular firm for the inspection. While the report came back with generally positive comments, there were many qualifiers in what an inspector had done or could comment. A qualified opinion on the wet wall should be intrepreted as a red flag of potentially a mould issue and require further due dilignece.

3. Manage your renovation budget - we originally budgeted for $5K, received quotes adding up $20K and ended up spending ~$15K. Granted, the house is old, no onsuite laundry facilities and dish washer, plus many other things that require potential upgrade. However, we learnt that we have to prioritize our spending, much more so than our home house. At the end of the day, what you want to do is to provide a safe, comfortable living space that looks attractive enough and leave a good first impression with the potential tenants. With that in mind, we crossed out items that are nice to have, but not must have (such as laundry, dish washer, yard), but focus on things that address the safety, comfort and first impression (such as humidifier, kitchen vent, stair, front porch). Plus, you can always leave some of the renovation item when the lease is up for renewal to appeal the tenants to stay for longer.

4. Beware of newly renovated unit - there is always a good or bad reason why the previous owner would spend $$ to upgrade the unit / house. It could be the owner hoping to make a significant premium, or even worse, hoping to cover up issue by some quick fix.

5. Try to get to know the neighbor before you buy - if you can. They are very good sources of due diligence of the current owner

Wednesday, November 17, 2010

REIN learnings Nov 16, 2010

1. Tenant evition

- critial info to get: sin, current phone, email, facebook, past landlord/employer, correct spelling of names (esp. Women w lots of last name)

- call landlord, ask for whether there are place to rent (to check real or not)

- parent contact - call it "in case of emergency contacts"

2. Carl Gomez fr Bentall

Marco:

-no inflation threat in next 5 years w lots of underutilized capacity

- canada: v shape recovery vs u-shape back in 90s. But growth coming off soon, affected by FX rate and slower growth of others

-Lending / residential mortgage

-home owner equity - 70% in canada vs 40% in Us

Housing mkt outlook

- going into balanced market

- according to house / rent ratio, 63% over value in Canada

- Toronto: 10% over valuation

- on long term avg, real estate should not grow faster than inflation (source: irrational exuberance). Here's Carl's blog. check it out.

Canadaeco.blogspot.com

Job prospect

- onatrio recovered 80% of job it lost, vs alberta - 40%

3. Condo myth Brian Persuad

- 20,000 condo registered since 2009

- 1/3 are listed for sell

- 25% enter into rental supply

- avg age 42 or higher

- mortgage need to qualify today though don't need for 4 yrs

- develpers must sell 80% to get financing

- 2005 - green belt limit availability of low rise

- 905 area condo could be attractive

4. Eviction - Ricketts Harris

-Useful links

Landlord sell help line 4165045190

-Ontario and california toughest tenancy registration

- always use written correspondence in communicating w tenants

- eviction forms/notice shouldn't be emailed only

- Giving notice s 43: set out reason, info tenant you will seek order if they do not leave, infor tenant that they are entitled to challenge order, keep a copy

- Annual/monthly tenancy: 60 days notice period

- critial info to get: sin, current phone, email, facebook, past landlord/employer, correct spelling of names (esp. Women w lots of last name)

- call landlord, ask for whether there are place to rent (to check real or not)

- parent contact - call it "in case of emergency contacts"

2. Carl Gomez fr Bentall

Marco:

-no inflation threat in next 5 years w lots of underutilized capacity

- canada: v shape recovery vs u-shape back in 90s. But growth coming off soon, affected by FX rate and slower growth of others

-Lending / residential mortgage

-home owner equity - 70% in canada vs 40% in Us

Housing mkt outlook

- going into balanced market

- according to house / rent ratio, 63% over value in Canada

- Toronto: 10% over valuation

- on long term avg, real estate should not grow faster than inflation (source: irrational exuberance). Here's Carl's blog. check it out.

Canadaeco.blogspot.com

Job prospect

- onatrio recovered 80% of job it lost, vs alberta - 40%

3. Condo myth Brian Persuad

- 20,000 condo registered since 2009

- 1/3 are listed for sell

- 25% enter into rental supply

- avg age 42 or higher

- mortgage need to qualify today though don't need for 4 yrs

- develpers must sell 80% to get financing

- 2005 - green belt limit availability of low rise

- 905 area condo could be attractive

4. Eviction - Ricketts Harris

-Useful links

Landlord sell help line 4165045190

-Ontario and california toughest tenancy registration

- always use written correspondence in communicating w tenants

- eviction forms/notice shouldn't be emailed only

- Giving notice s 43: set out reason, info tenant you will seek order if they do not leave, infor tenant that they are entitled to challenge order, keep a copy

- Annual/monthly tenancy: 60 days notice period

- List out Causes: if it's illegal activity, landlord has liability too. Make sure get police involved.

Sunday, November 7, 2010

Investing in US real estate - now or later

We have been thinking about investing in US real estate for almost 2 years.

True that, the 40+% drop in real estate value has been tempting, but the foreclosure inventory has also been a major concern. Some are predicting the current inventory will continue to drag on the real estate prices till end of 2011 while others predicting it will possibly take 103 months to liquidiate all the inventories in the current market.

On top of that, the tax and legal system for Canadian buying real estate in US is complicated to navigate. I haven't seen many articles that deal with this issue in great details except for these that touch on the basic.

Truila - What are the tax laws for Canadian buying real estate in Florida

Subscribe to:

Posts (Atom)